The Day a Rocket Company Rang a Bell

How a company that nearly died on a Pacific atoll became the largest IPO in history, and what it now wants to build above our heads.

The Opening Bell

Friday morning, 12 June 2026. Nasdaq MarketSite, Times Square.

For one second, the bell hangs silent.

On the wall behind the podium, the LED glass waits to change. Then the bell sounds, and the screens turn over to four white letters on black.

SPCX.

Outside, the same four letters wrap the tower and spill into Times Square, where tourists stop to photograph a rocket company’s name as if it were a movie poster. Two thousand miles away, in the flat heat of South Texas, Elon Musk marks the same moment from Starbase, where the company’s largest rockets are welded and stacked.

Two places. One ticker.

The stock had been priced at $135 a share the night before. It opens at $150. By midday it climbs into the $160s, then the $170s, pushing SpaceX past the $2 trillion mark and making Musk, at least on paper, the world’s first trillionaire. [1]

There are numbers that describe value, and numbers that make value feel unreal. A trillionaire is not only a financial milestone. It is a sign that the market has started assigning almost mythological weight to a company still trying to make machines survive fire, gravity and vacuum.

The IPO, initial public offering, is the moment a private company steps into the public market. For SpaceX, it was also something stranger: the moment a company built on rockets, satellites, artificial intelligence and old science-fiction promises became available to ordinary investors as a ticker symbol.

The numbers are the headline. They are not the story.

The story is that twenty-four years earlier, this company was three failed launches away from not existing at all.

Before the bell, there was a rocket. Before the rocket landed, there were rockets that did not.

And before the market funded the future, there was a fourth attempt.

What SpaceX Actually Is

For someone new to the company, SpaceX is easiest to misunderstand as a rocket company.

That is where the story begins, but not where it now ends.

Strip away the noise, and the original SpaceX idea was almost brutally simple: build rockets, launch them, land them, and launch them again.

That last part, land them, is the revolution.

For decades, rockets were treated like exquisite, expensive, single-use machines. Imagine building a Boeing 747, flying it once, and dropping it into the ocean. That was the absurdity SpaceX refused to accept. Falcon 9, the company’s workhorse rocket, was designed as a reusable two-stage vehicle for carrying people and payloads into orbit. [2]

Reusability changed the shape of the business. It made launch more repeatable. Repeatable launch made new markets possible. And those new markets gave SpaceX something most rocket companies never had: infrastructure that compounds.

Falcon 9 became the workhorse. Dragon began carrying cargo and crew to the International Space Station.

Starship became the larger future bet: a fully reusable system designed to carry heavy payloads, and eventually people, to Earth orbit, the Moon, Mars and beyond. [3]

And then came Starlink: thousands of satellites turning SpaceX from a launch provider into a connectivity company. Starlink’s promise is not poetic but practical: high-speed, low-latency internet in places where fibre, towers and traditional infrastructure struggle to reach. [4]

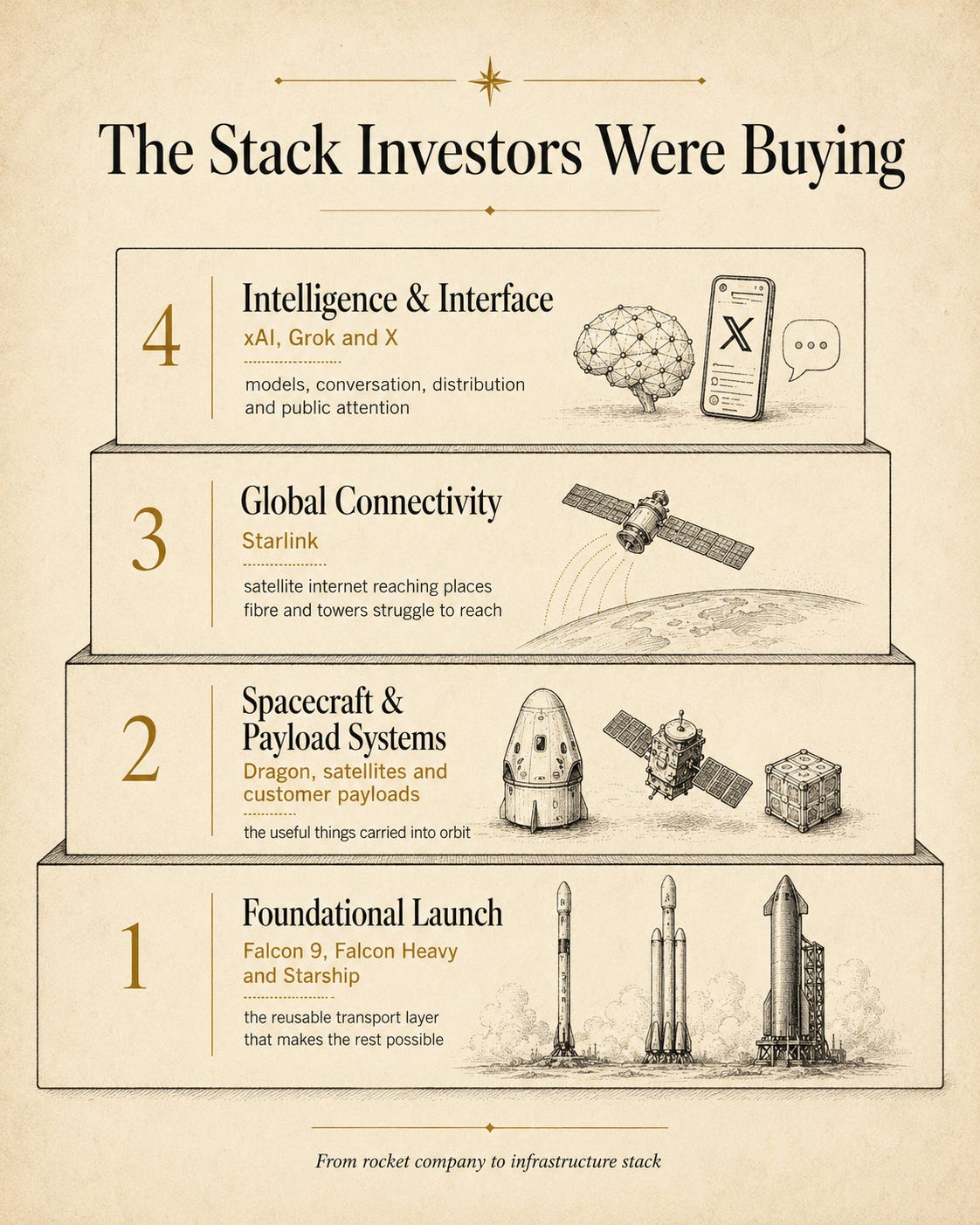

So by the time SpaceX reached the public markets, investors were not simply buying a rocket manufacturer.

They were buying a stack.

The Stack Investors Were Buying

That is the difference between the SpaceX private investors backed a few years ago and the SpaceX public investors were being invited to buy.

The old company was already extraordinary: reusable rockets, NASA missions, Starlink and Starship. But the listed company was stranger and broader. It was a bet that launch, satellites, connectivity, real-time information and artificial intelligence could become parts of the same machine.

A rocket company had become an infrastructure company.

And the infrastructure was no longer only physical.

The Furnace Years

In 2008, SpaceX was still a company with more ambition than proof.

Its small Falcon 1 rocket had launched three times from Kwajalein Atoll in the Pacific. All three attempts had failed. The money was nearly gone. Tesla, Musk’s other impossible company, was also under strain.

The fourth Falcon 1 launch came in September 2008.

This one reached orbit. [5] A few months later, NASA awarded SpaceX a $1.6 billion cargo resupply contract for flights to the International Space Station. [6]

The biggest initial public offering in history was not built on a clean upward curve. It was built on an organisation that survived the point where a neater story would have ended.

Three failures.

One more launch.

Then a contract.

Then a decade of making the unlikely look operational.

But SpaceX was not inevitable in 2008.

It was alive because the fourth rocket flew.

The Turn: xAI and X Come Aboard

The company that listed in June 2026 was no longer just SpaceX in the old sense. Its filing included xAI, acquired by SpaceX effective 2 February 2026, and X Holdings, acquired by xAI effective 28 March 2025. [7]

That means the public-market SpaceX is no longer rockets and satellites alone.

It is rockets, satellites, a global internet network, an artificial intelligence lab, and a real-time social platform sitting under the same corporate roof.

The logic is industrial. Artificial intelligence needs enormous amounts of compute. Compute needs power, cooling, chips, capital and distribution. SpaceX has launch capacity, satellite manufacturing, solar exposure in orbit, and now public-market capital. xAI brings the model-building ambition. X brings distribution, data, live conversation, attention and a daily interface with public culture.

It is also the same bet this company has always made: collapse separate industries into one machine and see whether the seams disappear.

Rockets did not have to stay disposable.

Internet did not have to stay cable-bound.

And now intelligence, perhaps, does not have to stay entirely Earth-bound.

That does not make the outcome certain. Orbital data centres remain an unsolved engineering and economic problem. xAI has been expensive to run. X carries its own regulatory and reputational baggage. And a merger between Musk-controlled companies is not something investors should treat as a fairy tale.

But it does clarify why the IPO commanded such demand.

The market was not pricing a rocket company.

It was pricing a vertically integrated attempt to build the infrastructure layer for the next technological age.

Why the Biggest IPO Ever

SpaceX raised $75 billion by selling roughly 555.6 million shares at $135 each, more than double the previous IPO record set by Saudi Aramco in 2019. [8]

That number is almost too large to feel human.

But the demand makes more sense when seen through two lenses.

First, SpaceX became one of the clearest public-market ways to buy into the convergence of space infrastructure and artificial intelligence. Most AI investment stories are still Earthbound: data centres, chips, cloud providers, model labs. SpaceX offered something more cinematic and more speculative: the possibility that launch, satellites, communications and compute could become part of the same system.

Second, SpaceX invited ordinary investors into the event more visibly than most marquee IPOs. Fidelity said SpaceX reserved up to 30% of the offering for retail investors, far above the usual 5% to 10% allocation in many IPOs. [9]

A company that spent two decades telling a public story about Mars, reusable rockets and human expansion did not want its market debut to feel entirely locked behind institutional doors.

The public was not just the audience. It was offered a small seat on the cap table. Still, the scepticism matters.

A company can be historic and expensive at the same time. Morningstar reported that SpaceX had a net loss of $4.93 billion on $18.67 billion of revenue in 2025, on a consolidated basis. [10] Reuters Breakingviews noted that the valuation depends heavily on future markets, AI infrastructure ambitions, and the belief that SpaceX can turn today’s technical dominance into tomorrow’s economic engine. [11]

That is the honest tension. SpaceX did not arrive at the market as a safe, boring business.

It arrived as a priced imagination.

A company with real rockets, real customers, real satellites, real contracts, and a valuation that still asks investors to believe in a future that has not fully happened yet.

But then, that has always been the SpaceX bargain.

In 2008, the future it was priced for was simply survival.

In 2026, the future it is priced for is infrastructure above Earth.

Back to the Bell

There is a detail from Friday worth keeping.

The bell was not only rung from a trading floor. It was also marked from Starbase, surrounded by the place where the company’s future is still being welded, tested, stacked, delayed, repaired and tried again.

That is the part no valuation model can fully capture.

For all the financial engineering, the merger terms, the share price, the retail allocation, the index speculation, the sudden paper wealth, the thing being sold on Friday was still tied to something older and rougher.

People trying to make a machine work.

People trying again after it did not.

People deciding a failure was not the end of the story.

The largest IPO in history did not begin with a bell.

It began with a fourth launch.

And the bell was only the echo.

Engineered by Gaurang is my reading room for technology, systems and stories, a place to understand not just what we build, but what our machines reveal about us.

Sources & Notes

[1] Reuters, “SpaceX soars 28% after record-busting IPO” reported SpaceX’s $150 open, first-day surge, and valuation moving above $2 trillion. The Guardian, “Elon Musk becomes world’s first trillionaire as SpaceX valuation passes $2tn” reported the paper-net-worth milestone.

[2] SpaceX, “Falcon 9” describes Falcon 9 as a reusable two-stage rocket designed to carry people and payloads into Earth orbit and beyond.

[3] SpaceX, “Starship” describes Starship as a fully reusable transport system for Earth orbit, the Moon, Mars and beyond.

[4] Starlink, “Technology” describes Starlink as a low Earth orbit satellite constellation designed to provide high-speed, low-latency internet.

[5] Reuters, “The road to SpaceX’s juggernaut IPO” covers SpaceX’s founding, Falcon 1’s 2008 orbital success, Falcon 9, Starlink and the IPO path.

[6] NASA Office of Inspector General, “NASA’s Commercial Cargo Providers” records SpaceX’s $1.6 billion Commercial Resupply Services contract for International Space Station cargo missions.

[7] SpaceX S-1 filing, SEC states that xAI was acquired by SpaceX effective 2 February 2026, and X Holdings was acquired by xAI effective 28 March 2025.

[8] Reuters, “Musk’s SpaceX prices record $75 billion IPO at $135 a share” reported the $75 billion raise, 555.6 million shares at $135, and the comparison with Saudi Aramco’s previous IPO record.

[9] Fidelity, “SpaceX IPO explained” says SpaceX reserved up to 30% of the offering for retail investors, compared with the more typical 5% to 10%.

[10] Morningstar, “6 Charts on SpaceX’s Pre-IPO Financials” reported a consolidated net loss of $4.93 billion on $18.67 billion of revenue in 2025.

[11] Reuters Breakingviews, “SpaceX’s $2 trln lift-off inaugurates new IPO era” framed the valuation risk around speculative future markets, AI infrastructure ambitions and investor belief in long-range plans.